A lot of investors don’t seem to talk about diversification. It’s easy to feel good about your investment prowess when the markets are continually rising and you’re making money almost regardless of what you invest in. But this attitude can come unstuck when market reversals happen (see recent market events) and in this post I want to stress the importance of spreading your risk. Bad times are always around the corner and being able to get through them is much easier with a diverse portfolio, even if it feels like you’re going against what everyone else seems to do.

Why do we need a diverse portfolio?

Among the most common pieces of advice for investors (at least it used to be) is that we should diversify our investments. But what actually counts as diversified? And how do we achieve good diversification without putting in a lot of effort and expense?

There are plenty of different ways, and the definition of diversified will vary depending on your individual circumstances, for example how risk averse you are, how large your portfolio is, and how long it will be before you need to access the money.

It’s your choice of course how to invest your money, but the best way to increase the value of your investments is steadily and slowly with minimal volatility. It’s the smart and long-term strategy that has a much higher success rate than the alternatives.

You’ll generally only hear stories from, and attention given to, the people who made a lot of money from their undiversified, hyper-volatile investment strategies, and not from the countless others who lost most of it because they didn’t diversify.

What does a diversified portfolio look like?

Quite simply, diversification is the spreading of risk in your whole portfolio into different investments that make it less likely that you’ll suffer extremely poor experience (or conversely benefit from extremely good experience) at the same time, when for example stock markets crash or bond yields drop etc.

The main ways to achieve diversification include:

- Geographically

- Multiple sectors/industries

- A range of company sizes/market capitalisations

- Different instrument types (e.g. money market, cash deposits at banks, equities, bonds, commodities, ETFs, foreign currencies, cryptocurrency)

- Owning both physical and non-physical assets (including using options and other leveraged instruments to track real assets)

- Full tracking of an index vs representative tracking

and many others.

I invest in index funds. I’m diversified, right?

I would wager that a lot of investors are not well diversified. Many buy individual stocks and an inadequate number of them across too few industries and geographies, so their returns are volatile. ETF and other fund holders are doing better in this respect, but I suspect most just hold one fund (the S&P 500 tracker), and ignore the other asset classes or don’t think about whether it diversifies enough for their own needs.

There is also a strong national bias towards owning assets in an investor’s own stock market, in many countries. This may actually be logical (and we are often incentivised to do this) since the funds are often cheaper in terms of fees, and there are not usually foreign exchange costs to consider and it’s therefore easier.

Owning the US market has been a highly profitable position over the last several years (arguably decades), and even owning the top 10 companies would have been enough to outperform almost everything globally. However, this is missing the point of diversification. The goal is to protect you against extreme downturns, and those top 10 US stocks and even the S&P 500 itself are not immune to market downturns.

As hard as it is, it may be worth feeling like you’re missing out on greater returns in order to achieve better diversification, because when it goes wrong you’re then not suffering as much as others who didn’t use caution.

What’s the point? Aren’t all asset classes correlated anyway?

To some extent this is true. Especially for the asset classes that most investors invest in: equities. People probably don’t get the diversification they would get if they also held currencies, commodities, and a higher proportion of bonds in their portfolios. If all you invest in is equities, you’re likely to see a lot of correlation between the returns of equities in your portfolio.

Economies and the performance of financial markets do appear to be more correlated now as the world’s financial centres, transport hubs, and trade links are more closely interwoven.

Just-in-time methods of manufacture and supply mean that events in distant countries can have knock-on effects on companies and stock markets far away overseas. e.g. chip manufacturing in Taiwan and the consumption of these chips by Apple based in the US.

Wars and political events around the world can have a meaningful effect on many asset classes globally at the same time. There’s also the possibility of trade wars and tariffs that highlight the fragility of our economic systems, and an accompanying flight to perceived safe havens to protect capital when these things happen.

How to achieve diversification

In theory, just owning the whole global market is the best diversification. A cheaper way of doing this may be owning as many companies as possible or a representative sample of companies. Index trackers are cheap and give large exposure. Fund managers are notoriously bad at outperforming the market or are at least no better than random chance, so the fees for actively managed funds may not be worth it.

Does an all-share ETF offer diversification? After all, it invests in all equities in the FTSE All world index, or all companies in the S&P 500. However, it does this in proportion to their market capitalisations, so the weighting is towards a smaller number of stocks.

The economy exhibits vast inequalities, similar to those in the personal income and wealth space. A very small number of companies in a concentrated sector produce the vast majority of the revenue, innovation, profit, and shareholder value, and have seen a similar proportion of the gains in share price and market value.

Therefore in order to get exposure to a representative sample of the whole index, practically speaking there’s no point in going to the trouble and expense of buying all the other 450 equities in the S&P500 because they don’t add much.

That logic would only break down if there was a catastrophic reduction in the tech sector and then the remaining companies would see an outsized inflow of capital as investors realised these assets were undervalued. It’s just hard to imagine this happening at the moment, and it would be brave to bet on it. The price of being wrong or early would be sitting on years of underperformance relative to other investors.

Ultimately, individual investors want to try to achieve the best possible diversification they can in the most cost-effective way, and ETFs do offer this.

1. Geographical diversity

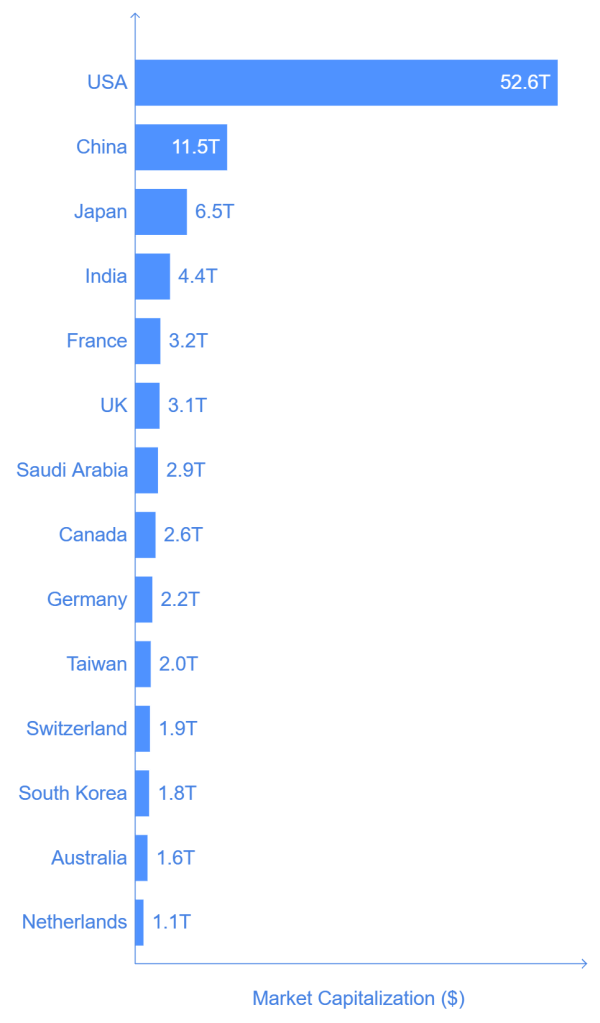

Bundling ETFs that cover the globe is a good strategy, but the difficulty lies in choosing the proportions. One method is the value of stock markets in each country or region. This data is provided in rough form in a few places, and I’ve it pieced together into one table below (data credit here):

You can see the US dominates, and with just seven companies accounting for 17 trillion dollars of the total. Based on this it would appear that skewing your investments towards the US is a decent strategy.

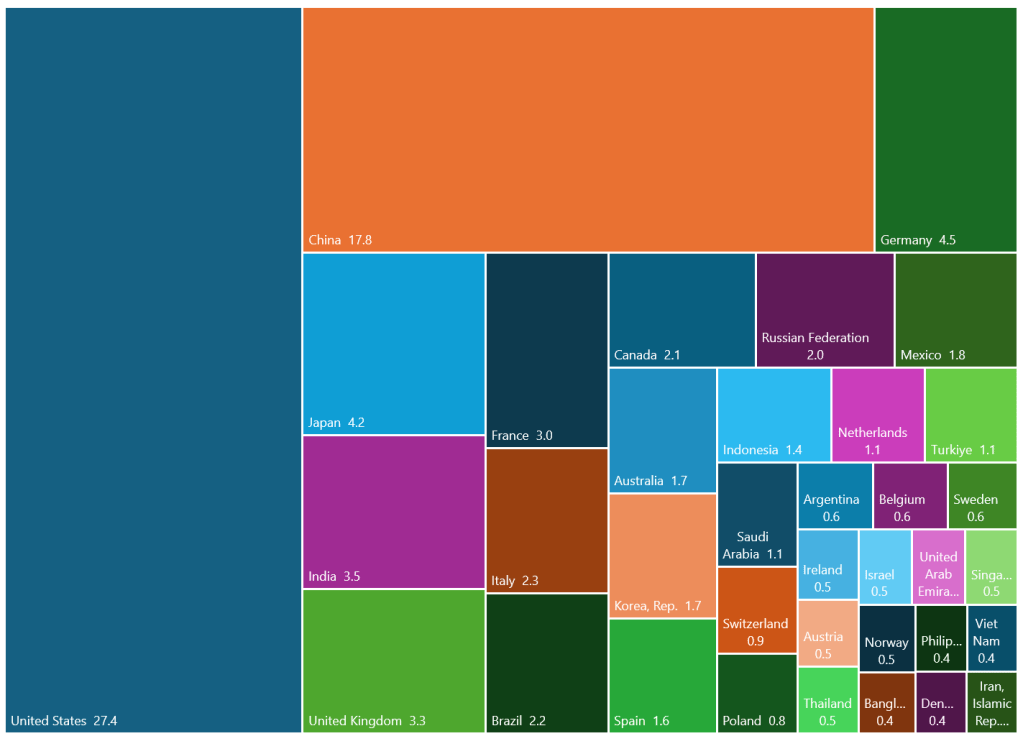

Or perhaps the sizes of economies as measured by GDP (this is 2023 data from the world bank, and it has been much more nicely visualised on 2019 data here), tells a similar story:

As you can see, heavily skewed. Therefore it’s probably best to use this as a starting point and define your own diversification goal and stick to that, e.g.

| Region | Proportion of world GDP |

| UK | 5% |

| USA | 60% |

| Japan | 5% |

| Europe ex UK | 10% |

| Asia ex Japan | 10% |

| China and Emerging Markets | 10% |

There’s a bit of bias in my choices above as I’m UK based and would like to hold a slightly higher proportion in my own country, but I admit this is arbitrary, especially given how poorly the UK market is performing, and how poor the investment horizon looks with the new government’s recent budget.

2. Market capitalisation

After geography, we then need to ensure we are happy with the market cap diversification. So we can add a small amount of small-cap funds to fill in the gaps, as a lot of the index funds will be weighted towards large established companies.

The vast majority of companies are in fact small companies (SMEs). Their turnover makes up over half of the total revenue of private companies in the UK for example.

Small cap funds do have the disadvantage of being more volatile and with higher expenses, so you have to do your own cost benefit analysis to determine if they add the right type of diversification for you.

3. Other asset classes

We can then add commodity funds (e.g. mining – precious metals like gold/silver, copper, uranium), but these tend to be more expensive to get exposure to and by some accounts (see previous post) commodities should make up a large proportion of our investments, which may be unfamiliar territory for a lot of individual investors.

Other major asset classes to consider include corporate and government bonds, property, and of course even some cash as a reserve. Portfolios should be skewing towards bonds, under the traditional advice, as you approach retirement anyway, but holding some bonds is good advice generally.

I’m not even going to go into cryptocurrency here, but some consider it to be a diversifying asset too.

Can you over-complicate diversification?

Remember that achieving diversification is not a set-and-forget activity. It needs adjustment periodically. For example, the age demographic of each country skews the asset class preferences over time (e.g. between equities and bonds), so what is diversified now won’t stay diversified forever, and also as prices fluctuate and countries’ economies and influence wax and wane there will be a need to rebalance.

It’s common sense that owning multiple companies in your portfolio as individual shares provides better diversification than holding one company. The effect improves quickly up to a point, of around 15 companies I seem to recall. Then the diversification effect tails off as diminishing returns overtakes.

Does the same apply with ETFs or other index fund tracking investments? Probably, to a lesser degree. The main problem is the time commitment of monitoring and maintaining it all each month as you make additions.

Stick to something simple and representative unless you have the resources and time to devote to finessing it. Having something invested regularly is better than doing nothing. Don’t let the problem of diversification stop you from investing at all. The options we have today for investing are a million times better than what was available not too many years ago, so the default ETF options are a decent bet and address a lot of the problems.

Summary

Diversification is an often overlooked but very important part of your investment strategy, but it can be complex and impractical to achieve. As long as you’re considering whether your portfolio is diversified for your needs you’ve made the first step that many appear not to make when they start investing.

It’s a highly individual issue which you’ll need to think about for yourself, but if you make sure that you incorporate different geographies, market capitalisations and asset classes in your portfolio whilst keeping the costs and time commitment down, that approach should serve you well.

Are there any other ways that you achieve diversification? Let me know in the comments. Thanks for reading.

Leave a reply to The problems with index funds – Exploratory Finance Cancel reply